Рус

Рус

RNC Pharma: Foreign Pharma Companies That Have Localized Production in Russia Contribute to Growth Rates in January–July 2024

In January–July 2024, Russia manufactured 462.5 billion rubles’ worth of finished pharmaceutical products (manufacturer’s prices, VAT included), up 16% from the same period last year. In physical terms, it was 2.37 billion packages, up 4.6% from January–July 2023. This time, every manufacturer’s contribution to the growth rates depended on the type of the company.

All pharmaceutical manufacturers in Russia can be divided into three types: foreign companies that have localized production in Russia (at their own and contract plants; these companies include Gedeon Richter, Novartis, Servier, etc.), foreign-owned Russian companies (Akrikhin, Veropharm, etc.), and fully Russian businesses (Pharmstandard, Binnopharm, Ozon, etc.). This classification is tentative, since ownership structure of certain companies is rather confusing, and ownership often changes. Russian manufacturers accounted for as much as 83.4% of production in physical terms in January–July 2024. An all-time-high, 86.6%, was seen back in 2020, when the pandemic led to a massive increase in the demand for the drugs included in the Temporary Guidelines for the Prevention, Diagnosis and Treatment of COVID-19. After that, the share of Russian companies decreased, although by just a few tenths of a percent. In January–July 2024, the manufacture by Russian pharmaceutical companies grew 5% from January–July 2023.

After a significant surge in 2021, the share of foreign-owned manufacturers in Russia remained practically the same for 2.5 years. In 2023, these companies accounted for around 7.6% of the total production against 7.3% in January–July 2024. There are not many foreign-owned Russian companies, and their manufacturing output fell 3.5% in physical terms from January–July 2023.

Foreign companies that have localized production in Russia contributed to the growth rates in January–July 2024 the most, accounting for 9.3% of the total manufacture. After a small decrease in 2022, which could possibly be associated with the sanctions and changes in the way of doing business in Russia, these companies started to grow again and have now been growing at an accelerated pace for more than 18 months. In 2023, their manufacturing output went up 3% from the previous year. In January–July 2024, the manufacture grew 8.9% from the same period last year, which determined the total growth rates.

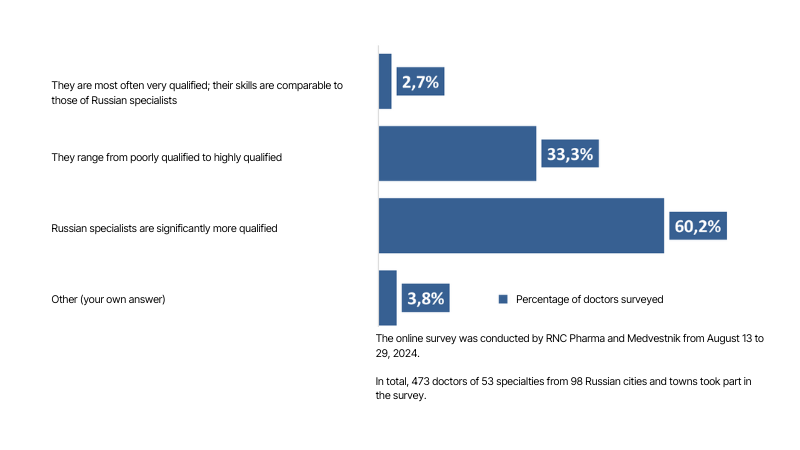

Fig. Pharmaceutical drug production structure in Russia, Russian and foreign companies, %, packages

*including manufacturing output of foreign companies at owned and contract plants